# AmeriOpt

A Python Package for Pricing American Option using Reinforcement Learning.

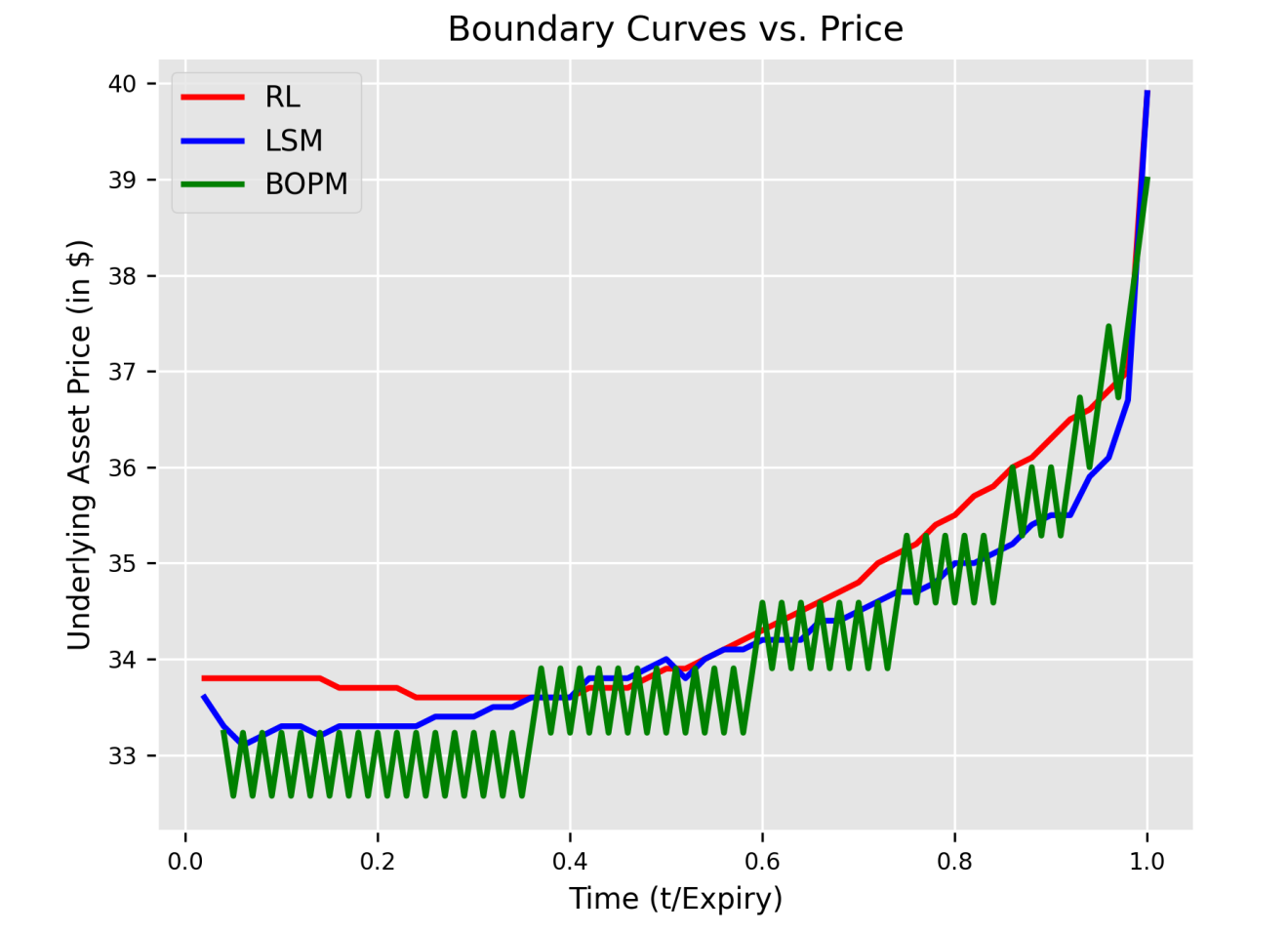

The full documentation of paper can be found in [https://www.mdpi.com/1999-4893/17/9/400](https://www.mdpi.com/1999-4893/17/9/400)

To use package, you need to follwo the following steps:

## Installation

```bash

pip install ameriopt

```

## Import the package

```python

from ameriopt.rl_policy import RLPolicy

```

## Set the parameters of GBM model

- Number of Laguerre polynomials to be used in the RL model

```python

NUM_LAGUERRE = 5

```

- Number of training iterations for the RL algorithm

```python

TRAINING_ITERS = 3

```

- Small constant for numerical stability in the RL algorithm

```python

EPSILON = 1e-5

```

- Strike price of the option

```python

STRIKE_PRICE = 40

```

- Time to expiration (in years)

```python

EXPIRY_TIME = 1.0

```

- Risk-free interest rate

```python

INTEREST_RATE = 0.06

```

- Number of time intervals

```python

NUM_INTERVALS = 50

```

- Number of simulations for generating training data

```python

NUM_SIMULATIONS_TRAIN = 5000

```

- Number of simulations for testing the RL policy

```python

NUM_SIMULATIONS_TEST = 10000

```

- Spot price of the underlying asset at the start of the simulation

```python

SPOT_PRICE = 36.0

```

- Volatility of the underlying asset (annualized)

```python

VOLATILITY = 0.2

```

## Simulate Training Data using Geometric Brownian Motion (GBM)

```python

training_data = simulate_GBM_training(

expiry_time=EXPIRY_TIME,

num_intervals=NUM_INTERVALS,

num_simulations=NUM_SIMULATIONS_TRAIN,

spot_price=SPOT_PRICE,

interest_rate=INTEREST_RATE,

volatility=VOLATILITY

)

```

## Instantiate the RLPolicy model with defined parameter GBM Price Model

```python

rl_policy = RLPolicy(

num_laguerre=NUM_LAGUERRE,

strike_price=STRIKE_PRICE,

expiry=EXPIRY_TIME,

interest_rate=INTEREST_RATE,

num_steps=NUM_INTERVALS,

training_iters=TRAINING_ITERS,

epsilon=EPSILON

)

```

## Train the RL Model and Get Weights (Weight for the optimal policy)

```python

weights = rl_policy.get_weights(training_data=training_data)

```

# Generate test data (GBM paths) for option price scoring

```python

paths_test = scoring_sim_data(

expiry_time=EXPIRY_TIME,

num_intervals=NUM_INTERVALS,

num_simulations_test=NUM_SIMULATIONS_TEST,

spot_price=SPOT_PRICE,

interest_rate=INTEREST_RATE,

volatility=VOLATILITY

)

```

## Option price

```python

option_price = rl_policy.calculate_option_price(stock_paths=paths_test)

```

## Print the calculated option price

```python

print("Option Price using RL Method:", option_price)

```

Raw data

{

"_id": null,

"home_page": "https://github.com/Peymankor/AmeriOpt",

"name": "ameriopt",

"maintainer": null,

"docs_url": null,

"requires_python": ">=3.10",

"maintainer_email": null,

"keywords": "pandas",

"author": "Peyman Kor",

"author_email": "kor.peyman@gmail.com",

"download_url": "https://files.pythonhosted.org/packages/f9/90/9ab66d66c25b22c6f057b5c6a22795f81ff99f4f294bbf8e6a826232ac43/ameriopt-0.1.5.tar.gz",

"platform": null,

"description": "# AmeriOpt\nA Python Package for Pricing American Option using Reinforcement Learning.\n\nThe full documentation of paper can be found in [https://www.mdpi.com/1999-4893/17/9/400](https://www.mdpi.com/1999-4893/17/9/400)\n\n\n\nTo use package, you need to follwo the following steps:\n\n## Installation\n```bash\npip install ameriopt\n```\n\n## Import the package\n\n\n```python\n\nfrom ameriopt.rl_policy import RLPolicy\n```\n\n\n## Set the parameters of GBM model\n\n- Number of Laguerre polynomials to be used in the RL model\n\n```python\nNUM_LAGUERRE = 5\n```\n\n- Number of training iterations for the RL algorithm\n\n```python\nTRAINING_ITERS = 3\n```\n\n- Small constant for numerical stability in the RL algorithm\n\n```python\nEPSILON = 1e-5\n```\n\n- Strike price of the option\n\n```python\nSTRIKE_PRICE = 40\n```\n\n- Time to expiration (in years)\n\n```python\nEXPIRY_TIME = 1.0\n```\n\n- Risk-free interest rate\n\n```python\nINTEREST_RATE = 0.06\n```\n\n- Number of time intervals \n\n```python\nNUM_INTERVALS = 50\n```\n\n- Number of simulations for generating training data\n\n```python\nNUM_SIMULATIONS_TRAIN = 5000\n```\n\n- Number of simulations for testing the RL policy\n\n```python\nNUM_SIMULATIONS_TEST = 10000\n```\n\n- Spot price of the underlying asset at the start of the simulation\n\n```python\nSPOT_PRICE = 36.0\n```\n\n- Volatility of the underlying asset (annualized)\n\n```python\nVOLATILITY = 0.2\n```\n\n\n## Simulate Training Data using Geometric Brownian Motion (GBM)\n\n\n```python\ntraining_data = simulate_GBM_training(\n expiry_time=EXPIRY_TIME,\n num_intervals=NUM_INTERVALS,\n num_simulations=NUM_SIMULATIONS_TRAIN,\n spot_price=SPOT_PRICE,\n interest_rate=INTEREST_RATE,\n volatility=VOLATILITY\n)\n```\n\n## Instantiate the RLPolicy model with defined parameter GBM Price Model\n\n```python\nrl_policy = RLPolicy(\n num_laguerre=NUM_LAGUERRE,\n strike_price=STRIKE_PRICE,\n expiry=EXPIRY_TIME,\n interest_rate=INTEREST_RATE,\n num_steps=NUM_INTERVALS,\n training_iters=TRAINING_ITERS,\n epsilon=EPSILON\n)\n```\n\n## Train the RL Model and Get Weights (Weight for the optimal policy)\n\n\n```python\nweights = rl_policy.get_weights(training_data=training_data)\n```\n\n# Generate test data (GBM paths) for option price scoring\n\n```python\npaths_test = scoring_sim_data(\n expiry_time=EXPIRY_TIME,\n num_intervals=NUM_INTERVALS,\n num_simulations_test=NUM_SIMULATIONS_TEST,\n spot_price=SPOT_PRICE,\n interest_rate=INTEREST_RATE,\n volatility=VOLATILITY\n)\n```\n\n## Option price\n\n```python\noption_price = rl_policy.calculate_option_price(stock_paths=paths_test)\n```\n\n## Print the calculated option price\n\n```python\nprint(\"Option Price using RL Method:\", option_price)\n```",

"bugtrack_url": null,

"license": "MIT",

"summary": "This is a package for pricing American options using reinforcement learning",

"version": "0.1.5",

"project_urls": {

"Homepage": "https://github.com/Peymankor/AmeriOpt",

"Repository": "https://github.com/Peymankor/AmeriOpt"

},

"split_keywords": [

"pandas"

],

"urls": [

{

"comment_text": "",

"digests": {

"blake2b_256": "12395a3c5ca0814cf72088d7fde5879ec26ec64ce02d910b5f1a8e508d513030",

"md5": "2ad09e5dcb2a077ab74edd07ca48b005",

"sha256": "e05bab4ec0a85b9c1215dbddbc9b838ccc09969db95d6251bd0ddc96efa29243"

},

"downloads": -1,

"filename": "ameriopt-0.1.5-py3-none-any.whl",

"has_sig": false,

"md5_digest": "2ad09e5dcb2a077ab74edd07ca48b005",

"packagetype": "bdist_wheel",

"python_version": "py3",

"requires_python": ">=3.10",

"size": 7402,

"upload_time": "2024-09-11T13:09:54",

"upload_time_iso_8601": "2024-09-11T13:09:54.491550Z",

"url": "https://files.pythonhosted.org/packages/12/39/5a3c5ca0814cf72088d7fde5879ec26ec64ce02d910b5f1a8e508d513030/ameriopt-0.1.5-py3-none-any.whl",

"yanked": false,

"yanked_reason": null

},

{

"comment_text": "",

"digests": {

"blake2b_256": "f9909ab66d66c25b22c6f057b5c6a22795f81ff99f4f294bbf8e6a826232ac43",

"md5": "e8517fb9870c91be0aa2b29ac1b46985",

"sha256": "992c54315da4a16a394c700927f74dd0b05646b11e61d0f2a782894b832456e9"

},

"downloads": -1,

"filename": "ameriopt-0.1.5.tar.gz",

"has_sig": false,

"md5_digest": "e8517fb9870c91be0aa2b29ac1b46985",

"packagetype": "sdist",

"python_version": "source",

"requires_python": ">=3.10",

"size": 6070,

"upload_time": "2024-09-11T13:09:55",

"upload_time_iso_8601": "2024-09-11T13:09:55.843804Z",

"url": "https://files.pythonhosted.org/packages/f9/90/9ab66d66c25b22c6f057b5c6a22795f81ff99f4f294bbf8e6a826232ac43/ameriopt-0.1.5.tar.gz",

"yanked": false,

"yanked_reason": null

}

],

"upload_time": "2024-09-11 13:09:55",

"github": true,

"gitlab": false,

"bitbucket": false,

"codeberg": false,

"github_user": "Peymankor",

"github_project": "AmeriOpt",

"travis_ci": false,

"coveralls": false,

"github_actions": false,

"lcname": "ameriopt"

}