# jquants-pairs-trading

[](https://pypi.org/project/jquants-pairs-trading/)

[](https://opensource.org/licenses/MIT)

[](https://codecov.io/gh/10mohi6/jquants-pairs-trading-python)

[](https://github.com/10mohi6/jquants-pairs-trading-python/actions/workflows/python-package.yml)

[](https://pypi.org/project/jquants-pairs-trading/)

[](https://pepy.tech/project/jquants-pairs-trading)

jquants-pairs-trading is a python library for backtest with japanese stock pairs trading using kalman filter, J-Quants on Python 3.8 and above.

## Installation

$ pip install jquants-pairs-trading

## Usage

### find pairs

```python

from jquants_pairs_trading import JquantsPairsTrading

import pprint

jpt = JquantsPairsTrading(

mail_address="<your J-Quants mail address>",

password="<your J-Quants password>",

)

pprint.pprint(jpt.find_pairs([3382, 4063, 4502]))

```

```python

[('3382', '4502')]

```

### backtest

```python

from jquants_pairs_trading import JquantsPairsTrading

import pprint

jpt = JquantsPairsTrading(

mail_address="<your J-Quants mail address>",

password="<your J-Quants password>",

)

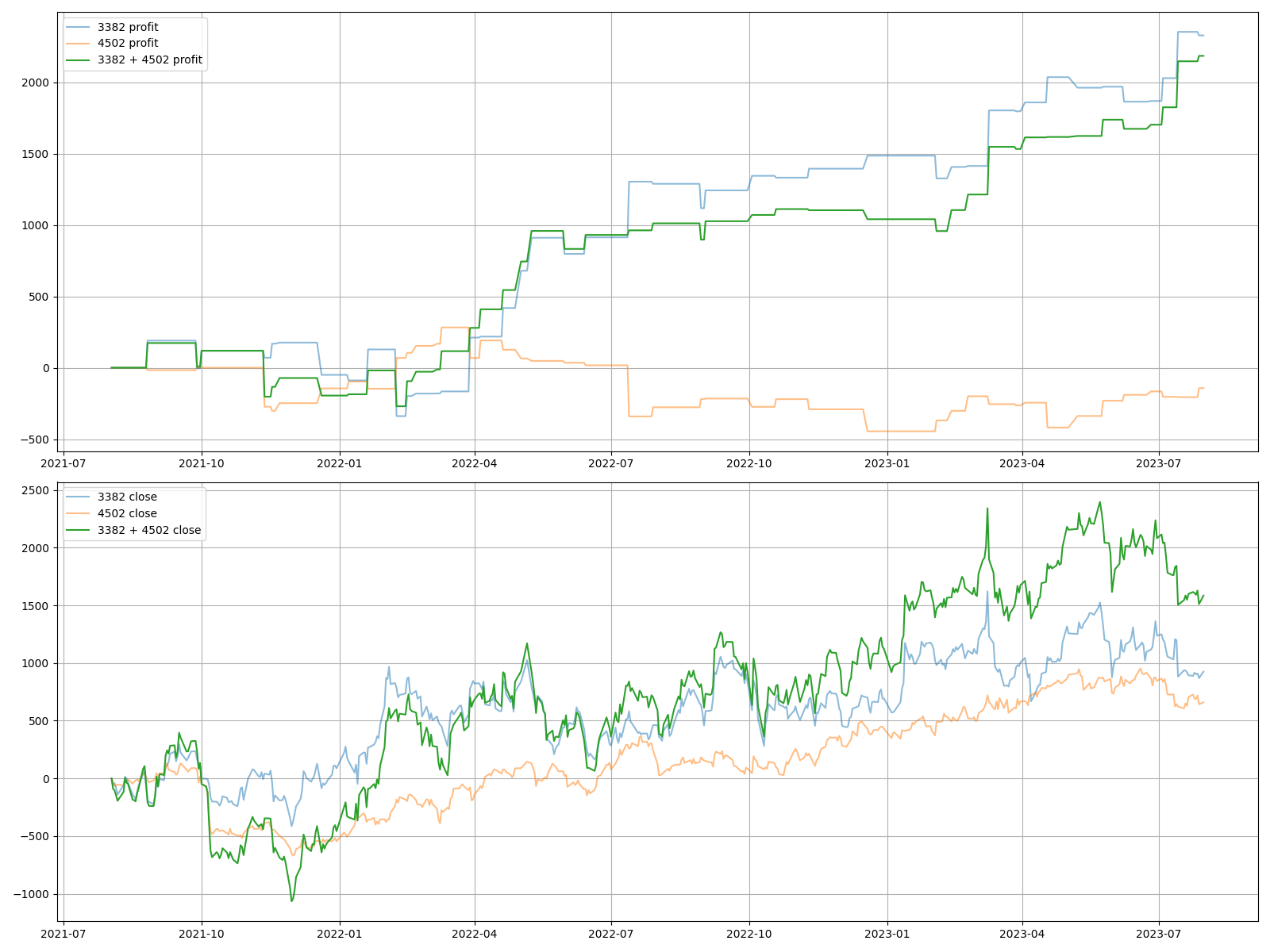

pprint.pprint(jpt.backtest((3382, 4502)))

```

```python

{'cointegration': '0.016',

'correlation': '0.814',

'maximum_drawdown': '443.000',

'profit_factor': '1.654',

'riskreward_ratio': '1.081',

'sharpe_ratio': '0.183',

'total_profit': '2184.000',

'total_trades': '86.000',

'win_rate': '0.605'}

```

### latest signal

```python

from jquants_pairs_trading import JquantsPairsTrading

import pprint

jpt = JquantsPairsTrading(

mail_address="<your J-Quants mail address>",

password="<your J-Quants password>",

)

pprint.pprint(jpt.latest_signal((6954, 6981)))

```

```python

{'6954 buy': True,

'6954 close': '4348.000',

'6954 long': False,

'6954 sell': False,

'6954 short': False,

'6981 buy': False,

'6981 close': '2775.000',

'6981 long': False,

'6981 sell': True,

'6981 short': False,

'date': '2023-07-31'}

```

### advanced

```python

from jquants_pairs_trading import JquantsPairsTrading

import pprint

jpt = JquantsPairsTrading(

mail_address="<your J-Quants mail address>",

password="<your J-Quants password>",

window=1,

transition_covariance=0.01,

pvalues=0.05,

zscore=0.5,

)

pprint.pprint(jpt.find_pairs([3382, 4063, 4502]))

pprint.pprint(jpt.backtest((3382, 4502)))

pprint.pprint(jpt.latest_signal((6954, 6981)))

```

## Getting started

For help getting started with J-Quants, view our online [documentation](https://jpx-jquants.com/).

Raw data

{

"_id": null,

"home_page": "",

"name": "jquants-pairs-trading",

"maintainer": "",

"docs_url": null,

"requires_python": ">=3.8",

"maintainer_email": "",

"keywords": "pairs trading,backtest,kalman filter,python,japanese stock,J-Quants,jquants",

"author": "",

"author_email": "10mohi6 <10.mohi.6.y@gmail.com>",

"download_url": "https://files.pythonhosted.org/packages/35/8d/f20b79856306793d53107e6bf93594c698e32b0be9100a295edfa4d22a82/jquants-pairs-trading-0.1.2.tar.gz",

"platform": null,

"description": "# jquants-pairs-trading\n\n[](https://pypi.org/project/jquants-pairs-trading/)\n[](https://opensource.org/licenses/MIT)\n[](https://codecov.io/gh/10mohi6/jquants-pairs-trading-python)\n[](https://github.com/10mohi6/jquants-pairs-trading-python/actions/workflows/python-package.yml)\n[](https://pypi.org/project/jquants-pairs-trading/)\n[](https://pepy.tech/project/jquants-pairs-trading)\n\njquants-pairs-trading is a python library for backtest with japanese stock pairs trading using kalman filter, J-Quants on Python 3.8 and above.\n\n\n## Installation\n\n $ pip install jquants-pairs-trading\n\n## Usage\n\n### find pairs\n\n```python\nfrom jquants_pairs_trading import JquantsPairsTrading\nimport pprint\n\njpt = JquantsPairsTrading(\n mail_address=\"<your J-Quants mail address>\",\n password=\"<your J-Quants password>\",\n)\npprint.pprint(jpt.find_pairs([3382, 4063, 4502]))\n```\n\n\n\n```python\n[('3382', '4502')]\n```\n\n### backtest\n\n```python\nfrom jquants_pairs_trading import JquantsPairsTrading\nimport pprint\n\njpt = JquantsPairsTrading(\n mail_address=\"<your J-Quants mail address>\",\n password=\"<your J-Quants password>\",\n)\npprint.pprint(jpt.backtest((3382, 4502)))\n```\n\n\n\n```python\n{'cointegration': '0.016',\n 'correlation': '0.814',\n 'maximum_drawdown': '443.000',\n 'profit_factor': '1.654',\n 'riskreward_ratio': '1.081',\n 'sharpe_ratio': '0.183',\n 'total_profit': '2184.000',\n 'total_trades': '86.000',\n 'win_rate': '0.605'}\n```\n\n### latest signal\n\n```python\nfrom jquants_pairs_trading import JquantsPairsTrading\nimport pprint\n\njpt = JquantsPairsTrading(\n mail_address=\"<your J-Quants mail address>\",\n password=\"<your J-Quants password>\",\n)\npprint.pprint(jpt.latest_signal((6954, 6981)))\n```\n\n```python\n{'6954 buy': True,\n '6954 close': '4348.000',\n '6954 long': False,\n '6954 sell': False,\n '6954 short': False,\n '6981 buy': False,\n '6981 close': '2775.000',\n '6981 long': False,\n '6981 sell': True,\n '6981 short': False,\n 'date': '2023-07-31'}\n```\n\n### advanced\n\n```python\nfrom jquants_pairs_trading import JquantsPairsTrading\nimport pprint\n\njpt = JquantsPairsTrading(\n mail_address=\"<your J-Quants mail address>\",\n password=\"<your J-Quants password>\",\n window=1,\n transition_covariance=0.01,\n pvalues=0.05,\n zscore=0.5,\n)\npprint.pprint(jpt.find_pairs([3382, 4063, 4502]))\npprint.pprint(jpt.backtest((3382, 4502)))\npprint.pprint(jpt.latest_signal((6954, 6981)))\n```\n\n## Getting started\n\nFor help getting started with J-Quants, view our online [documentation](https://jpx-jquants.com/).\n",

"bugtrack_url": null,

"license": "",

"summary": "jquants-pairs-trading is a python library for backtest with japanese stock pairs trading using kalman filter, J-Quants on Python 3.8 and above.",

"version": "0.1.2",

"project_urls": {

"Documentation": "https://github.com/10mohi6/jquants-pairs-trading-python",

"Homepage": "https://github.com/10mohi6/jquants-pairs-trading-python",

"Repository": "https://github.com/10mohi6/jquants-pairs-trading-python.git"

},

"split_keywords": [

"pairs trading",

"backtest",

"kalman filter",

"python",

"japanese stock",

"j-quants",

"jquants"

],

"urls": [

{

"comment_text": "",

"digests": {

"blake2b_256": "942afce3b87950c388ceb3646a70fe534ab14d8b5303d4f66f953826d5662ca5",

"md5": "47b4e0e16e77057e9551e481d33a5bf2",

"sha256": "6775748295ecc16c489f2829bd9b171e85afc87820eb076b5862c0cebc3a221a"

},

"downloads": -1,

"filename": "jquants_pairs_trading-0.1.2-py3-none-any.whl",

"has_sig": false,

"md5_digest": "47b4e0e16e77057e9551e481d33a5bf2",

"packagetype": "bdist_wheel",

"python_version": "py3",

"requires_python": ">=3.8",

"size": 6331,

"upload_time": "2023-10-30T14:27:50",

"upload_time_iso_8601": "2023-10-30T14:27:50.361581Z",

"url": "https://files.pythonhosted.org/packages/94/2a/fce3b87950c388ceb3646a70fe534ab14d8b5303d4f66f953826d5662ca5/jquants_pairs_trading-0.1.2-py3-none-any.whl",

"yanked": false,

"yanked_reason": null

},

{

"comment_text": "",

"digests": {

"blake2b_256": "358df20b79856306793d53107e6bf93594c698e32b0be9100a295edfa4d22a82",

"md5": "f1b21e1d924660a45b6f4ab4bccb41d1",

"sha256": "c92e79baf1931b9642ce93ebb16c5e4ecd16624ed2530cec0afdd248d8e11723"

},

"downloads": -1,

"filename": "jquants-pairs-trading-0.1.2.tar.gz",

"has_sig": false,

"md5_digest": "f1b21e1d924660a45b6f4ab4bccb41d1",

"packagetype": "sdist",

"python_version": "source",

"requires_python": ">=3.8",

"size": 6274,

"upload_time": "2023-10-30T14:27:53",

"upload_time_iso_8601": "2023-10-30T14:27:53.216459Z",

"url": "https://files.pythonhosted.org/packages/35/8d/f20b79856306793d53107e6bf93594c698e32b0be9100a295edfa4d22a82/jquants-pairs-trading-0.1.2.tar.gz",

"yanked": false,

"yanked_reason": null

}

],

"upload_time": "2023-10-30 14:27:53",

"github": true,

"gitlab": false,

"bitbucket": false,

"codeberg": false,

"github_user": "10mohi6",

"github_project": "jquants-pairs-trading-python",

"travis_ci": false,

"coveralls": false,

"github_actions": true,

"requirements": [

{

"name": "certifi",

"specs": [

[

"==",

"2023.7.22"

]

]

},

{

"name": "charset-normalizer",

"specs": [

[

"==",

"3.3.0"

]

]

},

{

"name": "contourpy",

"specs": [

[

"==",

"1.1.1"

]

]

},

{

"name": "coverage",

"specs": [

[

"==",

"7.3.2"

]

]

},

{

"name": "cycler",

"specs": [

[

"==",

"0.12.1"

]

]

},

{

"name": "exceptiongroup",

"specs": [

[

"==",

"1.1.3"

]

]

},

{

"name": "fonttools",

"specs": [

[

"==",

"4.43.1"

]

]

},

{

"name": "idna",

"specs": [

[

"==",

"3.4"

]

]

},

{

"name": "importlib-resources",

"specs": [

[

"==",

"6.1.0"

]

]

},

{

"name": "iniconfig",

"specs": [

[

"==",

"2.0.0"

]

]

},

{

"name": "jquants-api-client",

"specs": [

[

"==",

"1.5.0"

]

]

},

{

"name": "kiwisolver",

"specs": [

[

"==",

"1.4.5"

]

]

},

{

"name": "matplotlib",

"specs": [

[

"==",

"3.7.3"

]

]

},

{

"name": "numpy",

"specs": [

[

"==",

"1.24.4"

]

]

},

{

"name": "packaging",

"specs": [

[

"==",

"23.2"

]

]

},

{

"name": "pandas",

"specs": [

[

"==",

"1.5.3"

]

]

},

{

"name": "patsy",

"specs": [

[

"==",

"0.5.3"

]

]

},

{

"name": "Pillow",

"specs": [

[

"==",

"10.0.1"

]

]

},

{

"name": "pluggy",

"specs": [

[

"==",

"1.3.0"

]

]

},

{

"name": "pykalman-bardo",

"specs": [

[

"==",

"0.9.7"

]

]

},

{

"name": "pyparsing",

"specs": [

[

"==",

"3.1.1"

]

]

},

{

"name": "pytest",

"specs": [

[

"==",

"7.4.2"

]

]

},

{

"name": "pytest-cov",

"specs": [

[

"==",

"4.1.0"

]

]

},

{

"name": "pytest-mock",

"specs": [

[

"==",

"3.11.1"

]

]

},

{

"name": "python-dateutil",

"specs": [

[

"==",

"2.8.2"

]

]

},

{

"name": "pytz",

"specs": [

[

"==",

"2023.3.post1"

]

]

},

{

"name": "requests",

"specs": [

[

"==",

"2.31.0"

]

]

},

{

"name": "scipy",

"specs": [

[

"==",

"1.10.1"

]

]

},

{

"name": "seaborn",

"specs": [

[

"==",

"0.13.0"

]

]

},

{

"name": "six",

"specs": [

[

"==",

"1.16.0"

]

]

},

{

"name": "statsmodels",

"specs": [

[

"==",

"0.14.0"

]

]

},

{

"name": "tenacity",

"specs": [

[

"==",

"8.2.3"

]

]

},

{

"name": "tomli",

"specs": [

[

"==",

"2.0.1"

]

]

},

{

"name": "types-python-dateutil",

"specs": [

[

"==",

"2.8.19.14"

]

]

},

{

"name": "types-requests",

"specs": [

[

"==",

"2.31.0.6"

]

]

},

{

"name": "types-urllib3",

"specs": [

[

"==",

"1.26.25.14"

]

]

},

{

"name": "tzdata",

"specs": [

[

"==",

"2023.3"

]

]

},

{

"name": "urllib3",

"specs": [

[

"==",

"1.26.17"

]

]

},

{

"name": "zipp",

"specs": [

[

"==",

"3.17.0"

]

]

}

],

"lcname": "jquants-pairs-trading"

}